The global copper demand, driven by the green energy revolution and infrastructure projects, is facing a potentially debilitating supply crunch. With copper playing an essential role in renewable energy infrastructure, electric vehicles (EVs), and traditional industries like construction, electronics, and power generation, the pressure to meet the growing demand is mounting.

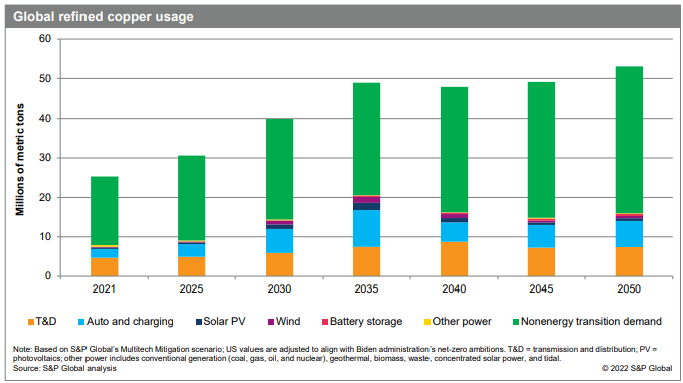

The S&P Global report from July 2022 predicts that by mid-century, the world will require 53 million tonnes of copper annually, more than double the current production of 21 million tonnes. As nations strive to reduce carbon emissions and achieve carbon neutrality by 2050, this ever-increasing demand for copper will put a strain on existing supplies and threaten to derail efforts to transition to renewable energy sources.

Source: S&P Global

One of the primary challenges in meeting this demand lies in the discovery and development of new copper deposits. As the largest copper mines face declining reserves and lower ore grades, maintaining current production levels becomes increasingly difficult. Furthermore, it takes an average of 16 years to develop a copper mine from initial discovery to production, according to the International Energy Agency. This means that even if new deposits are discovered today, it would take more than a decade to bring them into production.

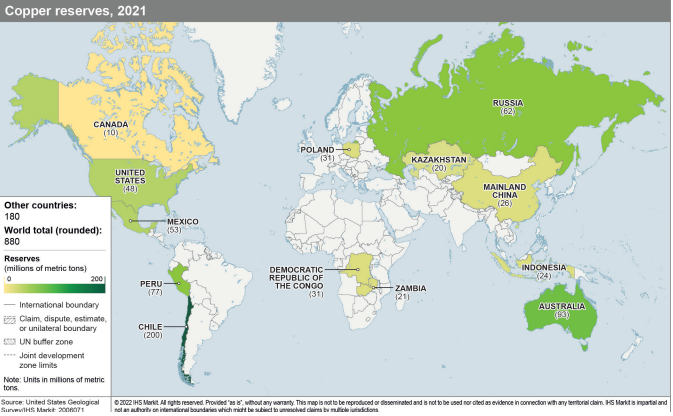

In addition, the geopolitical landscape surrounding copper production adds to the challenges faced in meeting demand. A significant amount of copper processing is concentrated in a few countries, including Chile, Russia, Australia, China, and several African nations. Environmental issues like water scarcity, flooding, and severe heat, as well as political factors like resource nationalism, sanctions and strict regulations, hamper the development and expansion of copper mines in these regions.

Chile, the world’s largest copper producer, is grappling with a water crisis that affects its ability to process sulphide ores which require large amounts of water. Furthermore, copper grades have dropped by 25% over the last decade, resulting in less ore being brought to market. Chile’s newly-elected leftist President Gabriel Boric has proposed higher taxes on the mining industry, which has raised concerns about the industry’s competitiveness.

Similarly, Peru, the second-largest copper producer, faces political uncertainty with the government still pondering an increase in taxes on the mining sector, potentially jeopardising future investments.

The current geopolitical tensions between the West and Russia are also poised to affect copper supply in the near future. As international relations become strained, trade restrictions and disruptions in the global supply chain could further exacerbate the copper deficit, placing even more pressure on the critical metal’s availability to various industries.

Source: S&P Global

Recycling copper is another potential avenue to address the supply gap. However, recycling currently represents a small fraction of the overall supply. In 2021, recycled copper accounted for just 4.5% of the total copper supply. While recycling efforts will continue to grow, they are unlikely to make a significant impact on the looming supply crunch.

In conclusion, the impending copper supply shortfall, coupled with the challenges of discovering and developing new copper deposits, and the limitations of recycling, underscores the potential opportunities in the copper sector, including trading copper futures.

Ivailo Chaushev,

Chief Market Analyst at Deltastock

Risk warning:

This article is for information purposes only. It does not post a buy or sell recommendation for any of the financial instruments herein analysed.

Deltastock AD assumes no responsibility for errors, inaccuracies or omissions in these materials, nor shall it be liable for damages arising out of any person’s reliance upon the information on this page.

73% of retail investor accounts lose money when trading CFDs with this provider.